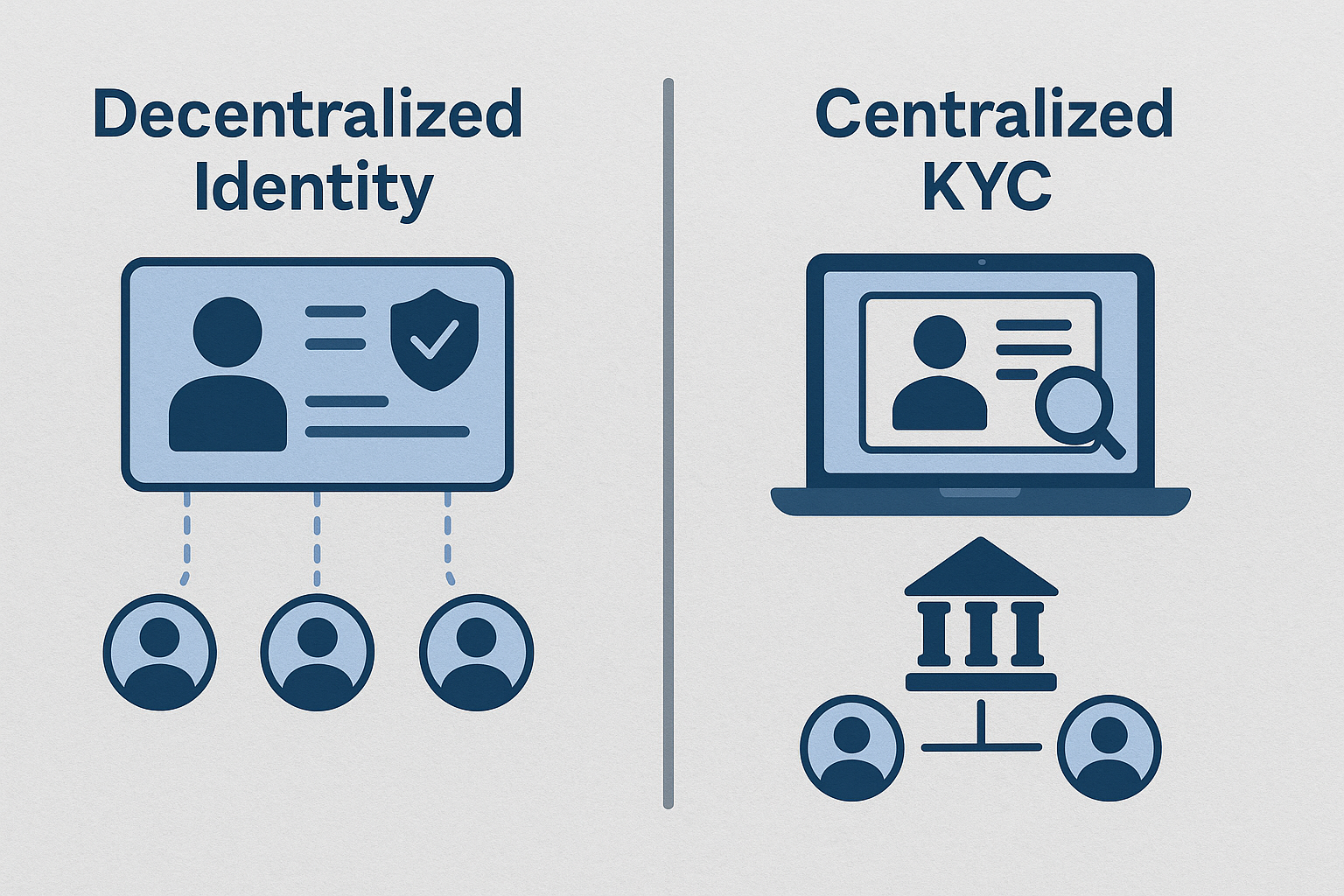

The fintech landscape is evolving at lightning speed, and one of the biggest debates today revolves around identity verification. Traditionally, Know Your Customer (KYC) processes have been centralized, where banks and financial institutions hold and control customer data. But with the rise of blockchain and Web3 technologies, decentralized identity (DID) is emerging as a strong alternative.

For fintech startups and established players alike, choosing between centralized KYC and decentralized identity is more than a technology decision—it impacts security, compliance, customer trust, and long-term scalability. Let’s dive into both models, compare their strengths, and explore which one might be the right fit for your fintech platform.

Understanding Centralized KYC

Centralized KYC is the system most financial organizations currently rely on. In this model, customer data is collected, stored, and maintained by a centralized authority—usually banks, credit bureaus, or government entities. For example, when a customer signs up for a new trading account, they upload their documents to the company’s servers. That company then becomes the custodian of the customer’s sensitive data.

Advantages of Centralized KYC

- Regulatory Compliance: Most global regulators recognize centralized KYC systems and already have frameworks in place.

- Faster Integration: Startups can use pre-built APIs from providers like Onfido, Jumio, or government-approved platforms.

- User Familiarity: Customers are used to uploading documents like passports or driver’s licenses for financial services.

Challenges with Centralized KYC

- Data Breaches: Centralized storage is a single point of failure. Cyberattacks on banks and fintechs have exposed millions of records in recent years.

- Costly Maintenance: Constant updates, server monitoring, and compliance management increase operational costs.

- Limited Portability: Customers often repeat the KYC process across platforms, leading to poor user experiences.

The Rise of Decentralized Identity (DID)

Decentralized identity, powered by blockchain, gives individuals ownership of their personal information. Instead of uploading documents to every new fintech app, customers can create a digital wallet with verifiable credentials. They control what information is shared, and the platform only validates the credentials, without storing them centrally.

Advantages of Decentralized Identity

- Data Ownership: Customers have complete control, reducing the risk of mass breaches.

- Interoperability: Once verified, credentials can be reused across multiple fintech platforms.

- Transparency: Blockchain ensures secure, auditable, and tamper-proof verification.

- Cost Savings: Reduces compliance overhead by eliminating duplicate checks.

Real-World Example

Microsoft’s ION Network and initiatives like Sovrin are leading decentralized identity projects. A textile export startup in Dallas recently integrated DID wallets for supplier verification, cutting onboarding time from 5 days to 30 minutes—a real productivity boost.

Which Model Fits Fintech Platforms Best?

The choice depends on business type, target audience, and compliance obligations.

- For Startups with Limited Resources: Centralized KYC is quicker to implement using existing providers.

- For Platforms Targeting Global, Digital-First Users: Decentralized identity is future-proof, aligning with Web3 and cross-border fintech adoption.

- Hybrid Approach: Some fintechs are combining both models—using centralized KYC for regulatory compliance while offering decentralized wallets for faster re-verification across services.

Industry Trends and Use Cases

- Crypto Exchanges: With rising regulatory scrutiny, many exchanges still depend on centralized KYC but are exploring DID for faster cross-platform onboarding. This is especially relevant as Crypto trading bot development services in Dallas expand, enabling automated trading platforms that still require strict compliance.

- Lending Platforms: AI-powered credit checks can integrate with DID systems. For instance, AI development services Dallas are already building models that connect decentralized identities with AI Predictive Models to assess borrower risk more accurately.

- Payments & Remittances: DID can drastically cut transaction delays caused by repeated KYC checks while ensuring security.

- Institutional Trading: Advanced fintechs using Custom Crypto Trading Bots are also leveraging DID to create seamless, compliant, and secure ecosystems for institutional clients.

Challenges of Implementing Decentralized Identity

- Regulatory Uncertainty: Many regulators still prefer centralized systems due to established laws.

- Technical Complexity: Building a decentralized identity system requires expertise in Web3 and blockchain.

- User Education: Customers need to adapt to digital wallets and self-custody models.

Despite these challenges, industry momentum shows DID adoption is rising, especially as enterprises prioritize privacy, interoperability, and data security.

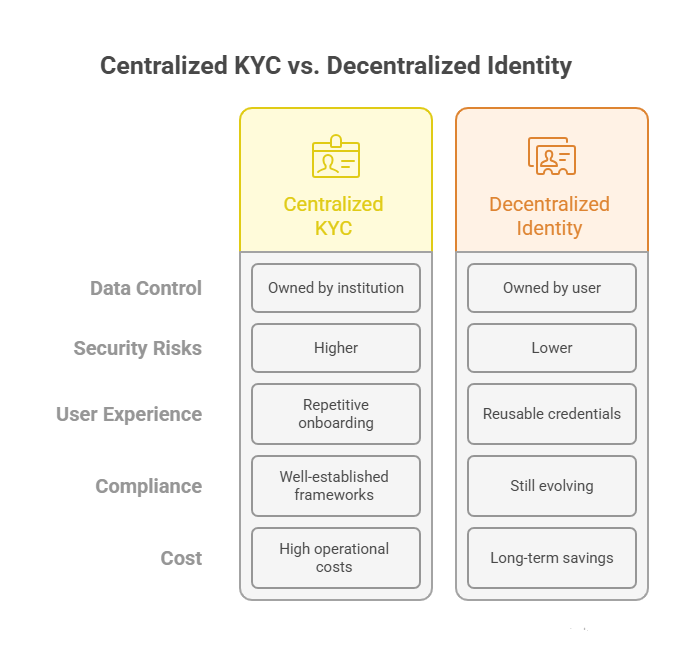

Centralized KYC vs. Decentralized Identity: A Quick Comparison

What the Future Holds

The future of fintech will likely not be fully centralized or fully decentralized. Instead, hybrid identity verification models will dominate, allowing platforms to stay compliant while delivering a seamless customer experience.

As more fintechs integrate Web3 infrastructure, decentralized identity will play a critical role in shaping cross-border payments, crypto adoption, and AI-driven risk assessments.

Conclusion

Both centralized KYC and decentralized identity bring unique benefits to fintech platforms. Centralized systems are more regulatory-ready, while decentralized identity promises future scalability and user empowerment. The best choice depends on your target market and long-term vision.

At Theta Technolabs, we help fintech businesses evaluate, design, and implement cutting-edge identity solutions across Web, Mobile and Cloud. Whether you’re exploring AI-driven risk analysis, decentralized blockchain solutions, or hybrid models, our team ensures your fintech stays ahead of the curve.

As a leading Web3 Development Company in Dallas, we specialize in creating secure, scalable solutions that align with compliance and customer needs.

📩 Get in touch today: sales@thetatechnolabs.com

Transform Your Fintech Identity System Today

Choosing between centralized KYC and decentralized identity can define your fintech platform’s success. Whether you’re looking to enhance compliance, improve security, or deliver a frictionless user experience, the right technology partner makes all the difference.

.png)

.png)

.png)

.png)

.png)

.png)